INTERNATIONAL TAXATION COMPARATIVE

THE REAL ESTATE TAXATION FRANÇAISE:

ONE OF THE MOST PERFORMING REGIMES

The fashion of the "french bashing" which is developing throughout Europe does not spare the field of taxation. France suffers from the rather negative image conveyed by the foreign media, without actually demonstrating it. The example of the tax at 75% of revenues which serves as their flagship argument for denouncing this excessive taxation is the most egregious example of this unfounded image. In this regard, we regularly find articles on websites, in foreign newspapers, even though this tax has been purely and simply deleted for individuals! It only concerns companies paying their employees an annual remuneration higher than one million euros. In the end, only 1,000 people in France will be affected by this tax through their company ...

France's reputation in terms of taxation is unfounded, particularly in the field of real estate.

France has nothing to envy to the real estate taxation of our European and American neighbors, which is at least as expensive if not more than in metropolitan France. Indeed, the acquisition of second homes are not more fiscally expensive in France and you should know that there are often unknown tax regimes that make investment property in France very attractive.

Because we are convinced that France's reputation in real estate taxation is unfounded, we propose to examine and compare objectively the tax burden related to investment in a second home by a non-profit. reside in France at our main European neighbors as well as in Florida. We specify that this comparative analysis does not take into account local taxes, the criteria for determining them being totally different according to the country and therefore incomparable objectively.

ACQUISITION COSTS

In France, they are estimated at about 7% of the value of the property. This rate includes all legal costs related to the acquisition, namely notary fees and various administrative procedures.

In our English neighbors, the acquisition costs are between 0 and 12% of the acquisition price according to scale. For "high-end" goods above £ 1,500,000, the rate is 12%, which is higher than the French rate. These fees do not include the fees of the "conveyancer": lawyer / lawyer responsible for performing various cadastral searches and other administrative procedures. His fees represent between 0.5 and 1% of the purchase price of the property.

As for Italy, it is estimated that the cost of acquiring a property by non-residents amounts to between 10% and 15% of the purchase price, not counting the fees of any legal adviser.

The acquisition in Spain assumes in the first place to "take out" the good of the market and to reserve it, with the payment of a deposit of between 3,000 and 6,000 €. This follows the payment of a transfer tax on the properties (ITP) between 8 and 11% of the purchase price ...

Therefore, we note that the rate of 7% practiced in France and including all legal fees is in the European average.

In Florida, it is clear the remarkable effort on acquisition costs that are estimated between 3 and 5% of the purchase price only.

TAXATION ON RENTAL INCOME

In France, it is taxed, for a non-resident, at the minimum rate of 20%, plus a tax on social security contributions of 15.5% (tax most certainly eliminated in the near future, see below). These tax rates may seem high, however, French tax law allows the deductibility of a large number of charges to substantially reduce the tax base.

These include depreciations that are deductible in seasonal furnished rental and allow a tax base almost zero.

In Florida, a non-resident alien will be taxed at the minimum rate of 30%.

In Italy, many expenses are also deductible but capped at 15% of rents.

The English also provide a tax regime favorable to seasonal rentals by granting an additional deduction of 10% of net rent ... But it remains less advantageous than the French regime!

We can also note the originality of Spanish and Swiss taxation. Indeed, in these two countries a tax on rental income is due ... even though the property is not rented!

This tax simply taxes the fact of enjoying one's property, even if it yields no income. Such a "fiscal fiction" does not take place in France and it would rightly be called a confiscatory tax.

TAXATION ON WEALTH

In France, it is due when the net worth of the taxpayer exceeds the threshold of 1.300.000 €. However, there are many ways to reduce the value of net taxable wealth below this threshold, especially for non-residents.

In Spain, this threshold is much lower because the tax is due from € 700,000 net worth and the highest portion of the scale is taxed at 2.5% (the highest French rate is only 1%). 5%).

Some countries tax wealth from the first euro

In Switzerland, for example in Geneva.

Others use devious ways to tax you

The United States does not know the wealth tax, but they apply a similar and specific tax on real estate: the property tax.

The tax rates are fixed by the states, in Florida it amounts to 2% of the market value!

Compared to French ISF, this tax proves to be more expensive: its rate is higher than the maximum rate of EWB in France and applies uniformly from the first dollar. The ISF in France is not ultimately so abusive as it is claimed. Simple solutions exist to reduce it, or even to completely eliminate it.

However, we can not deny the certain advantage of Italy and the United Kingdom. Indeed none of these countries tax the heritage.

TAXATION ON CAPITAL GAINS ON RESALE

When reselling, the tax rate of real estate capital gain in France is 34.5% (19% tax and 15.5% social security) for European residents. However, it is worth mentioning the recent conviction of France concerning the subjection of non-residents to social security contributions (CJEU judgment of 26 February 2015). In the long term, a non-resident investor would therefore be taxed at only 19% when reselling his property.

In addition, the calculation of the capital gain provides numerous discounts. A 7.5% abatement for acquisition costs and a 15% abatement for works are applied first (for buildings built and held for more than 5 years, deductions calculated on the purchase price). ). These fees may also be included for their actual amounts, subject to conditions.

Added to this is an allowance for the holding period of the building equal to 6% per year from the fifth year of detention (a ten-year holding will therefore allow a 30% reduction). The capital gain is therefore totally exempt from tax after 22 years of detention. France has returned to a more advantageous system, since previously the exemption from income tax was acquired after 30 years of detention.

Finally, although the rates are still high, the application of the many allowances provides a very low tax base and consequently a most reasonable tax.

For its part, the United Kingdom taxes capital gains on properties up to 28% for any capital gains exceeding £ 32,010 (approximately EUR 40,600).

Geneva applies a rate determined according to the duration of ownership of the building, which will be equal to 50% in case of resale after a detention of less than 2 years, 40% for a detention between 2 and 4 years, 30% between 4 and 6 years, and so on in a linear fashion. The exemption from tax on the capital gain of the property comes after 25 years of detention, ie 3 years after France.

In Florida, certain expenses are deducted from the acquisition value, which has the effect of increasing the tax base. Thus, although the 15% tax rate seems low, it applies to a very high base.

To conclude it is necessary to remember that a tax is calculated from a rate and a tax base! The media, often novices in the field, are only based on rates to denounce excessive French taxation.

As a result, these analyzes are not at all objective, since they do not take into account the base on which the rate must apply!

An in-depth examination leads to the understanding that high rates do not necessarily lead to high taxation, as the demonstration was made in this study.

This analysis is based on the "common law" regime, which would apply to an individual wishing to acquire a property as a second home.

It can be seen that the acquisition of a property in France is not more tax-intensive than in another European country and is instead rather advantageous.

It should be known that it is possible to further improve the "tax" profitability of its investment in France. Indeed, there is an "investor type" regime, which is particularly interesting. This scheme allows the obtaining of tax benefits, and consequently the improvement of rental profitability. The main advantages of this "investor" plan are summarized in the box below.

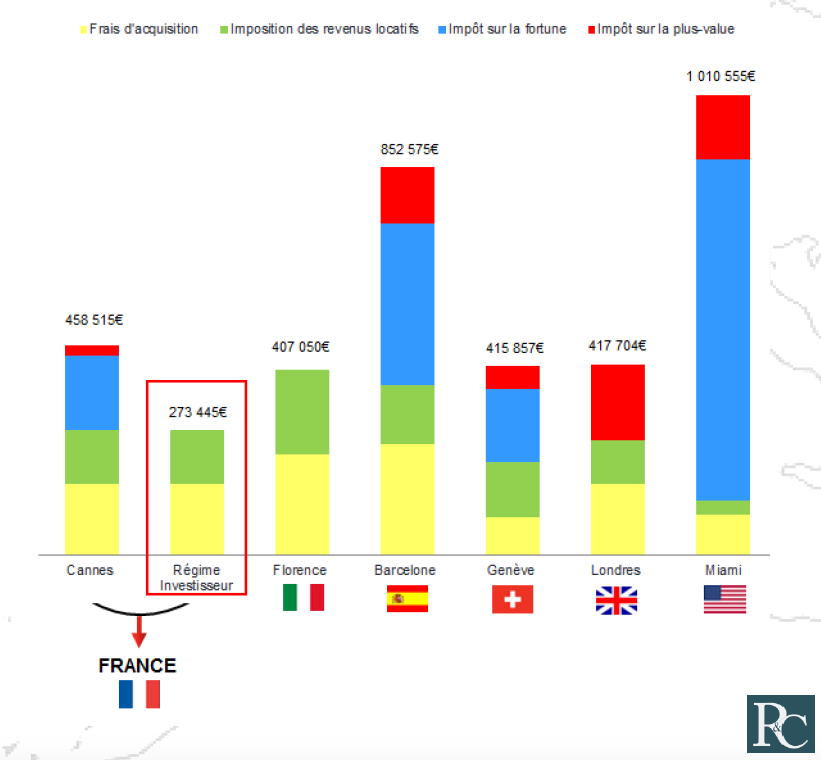

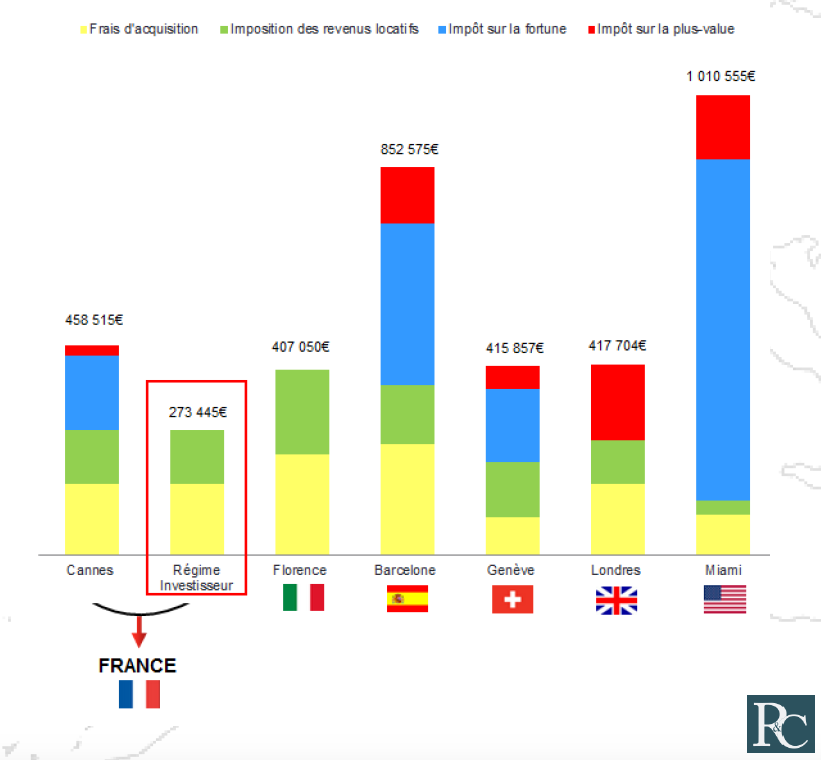

AN EXAMPLE IN FIGURE :

A Belgian couple, married, parent of two minor children acquires a villa for 2.2 million euros (equity financing).

The couple wants to rent the villa for three months in the summer (June, July and August).

Gross rental income: 50,000 euros.

Current expenses of the villa for the period (electricity, water, heating, property taxes, insurance, expenses of maintenance and various repairs ...): 15.000 euros.

Resale of real estate after 15 years of detention for 2.8 million euros.

The couple hesitates between several destinations: Cannes in France, Florence in Italy, Barcelona in Spain, Geneva in Switzerland, London in the United Kingdom and Miami in the United States.

They would like to know the tax impact of their investment in each of these destinations. Cost of operations calculated on a 15-year basis, with constant taxation (data Dec. 2014). The regimes of the different countries will be compared with an investment made in France through the "Investor" plan.

Source : Cabinet Roche & Cie, Expert-comptable à Lyon - Spécialiste de l‘immobilier et de la fiscalité des non-résident

Copyright 2017 SAS BENJAMINPRATT - Any reproduction prohibited